14 More Tips from a Financial Advice Industry Insider 14 More Tips from a Financial Advice Industry Insider

Some content could not be imported from the original document. View content ↗

2021年8月19日

∙ Paid

I hope you enjoyed the article from earlier this week, Investing: The Few Key Things You Need to Know. At least two of you started investing after reading it. I’m glad to hear! This is the follow-up, where we’re going to cover all these topics:

The FIRE Movement (Financial Independence; Retire Early)

The importance of negotiation in all of this

Fk Y Money: what it is, and what’s your number

How financial advisors create urgency

Cryptocurrencies, Fiat Currencies, Modern Monetary Theory (MMT), and how they affect all of this

When should you concentrate your bets?

Markovitz’ Efficient Frontier

What does diversification really mean?

Dollar-cost averaging

The mental biases that make active investing really hard

Specifics of tax optimization

The accelerating impact of returns

What parts of the work of a financial advisor can be automated

What the people working inside the roboadvice industry think about their products and how people invest

1. FIRE (Financial Independence; Retire Early): What Is It? Is It Worthwhile?

FIRE is more a movement than simple investment advice. It’s a lifestyle. The adherents try to save as aggressively as they can—up to 70% of their income—mostly by reducing their costs, investing that money, and then retiring as soon as they can by living off of the income generated by the investments.

There’s a lot of wisdom in that. You should be frugal [1] . Investing wisely is also great advice. Knowing when you can retire is intelligent.

But it has been pushed to such an extreme, that for many FIRE is to live a shitty life for some time so you can live a shitty life forever.

The FIRE movement says the entire goal of the savings period is to make money as fast as possible to quit your job. Which assumes the job is not something you can enjoy, because you’re not free. Because your job is assumed to be a grind, it takes away from your enjoyment. It also makes it so much harder to invest yourself in it, which is the best way to actually increase your income, which would get you closer to your goals.

While you do the work and saving, you don’t enjoy anything in life because you need to spend as little as humanly possible.

Do that until you can retire as soon as possible, which means your costs after retirement must be as low as possible because you’re living off of very little money. And since you’ve centered all your life around producing money to get your freedom, you’re now out of hobbies and enjoyment of life.

Personally, I prefer a more measured approach. Yes, be thrifty and invest wisely. But focus on today, too. Enjoy your life. It’s short. Understand that it’s ok to depend on others for parts of life. It’s part of the challenge of living in society and depending on each other. Spend on the small things that make you happy. Avoid expensive items. Don’t look at work as a torture to escape from, but rather figure out ways to align your interests with your job over time. Think about what you would want to do once you have the freedom to retire, and start doing that now.

And focus on increasing your income! By working harder, by enjoying your job, by trying things you enjoy on the side. And by negotiating.

2. The Importance of Negotiation

If investing is the most important thing to do for retirement, negotiating is the 2nd most important thing. I will write articles about this in the future, but in the meantime, here’s why it’s so important.

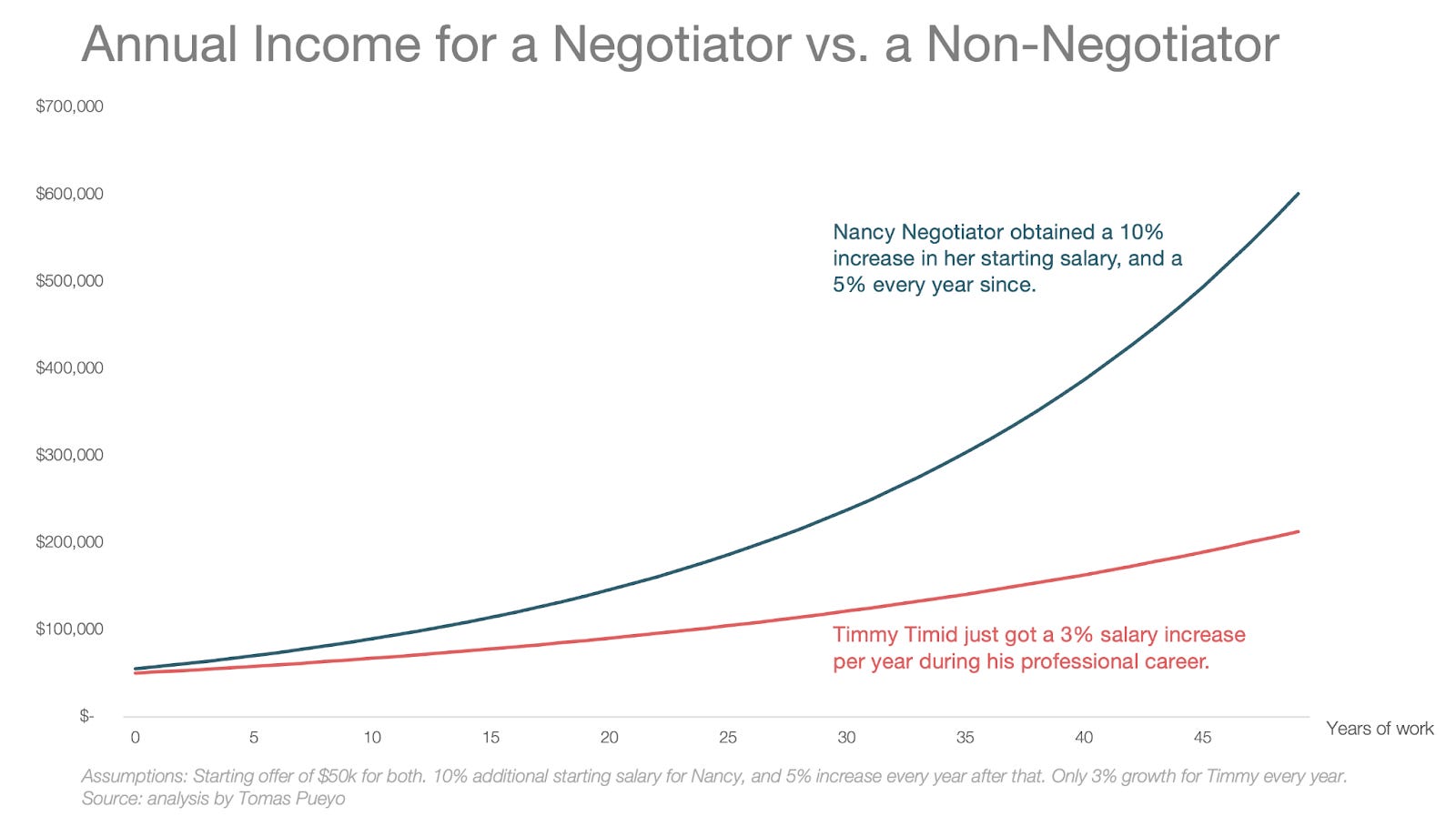

Imagine two people. Timmy Timid is a bit of an introvert, and he doesn’t like confrontational situations. Simply thinking about negotiating makes him sweat. In any case, he believes his work should speak for himself, so he expects his bosses to pay him what he’s worth. “If they don’t, I’ll just leave!” he tells himself. He waits for companies to reach out to him, though. Throughout his 50-year career, he will get an annual increase of about 3%, slightly above the inflation rate of 2%, reflecting his higher productivity.

Nancy Negotiator doesn’t believe that. She demands what she thinks her work is worth. Fresh out of college, she secured a 10% increase to her starting salary, and every year she’s managed to increase her salary by 5%.

When Timmy and Nancy retire, how much of a difference do you think this small difference has made in their incomes?

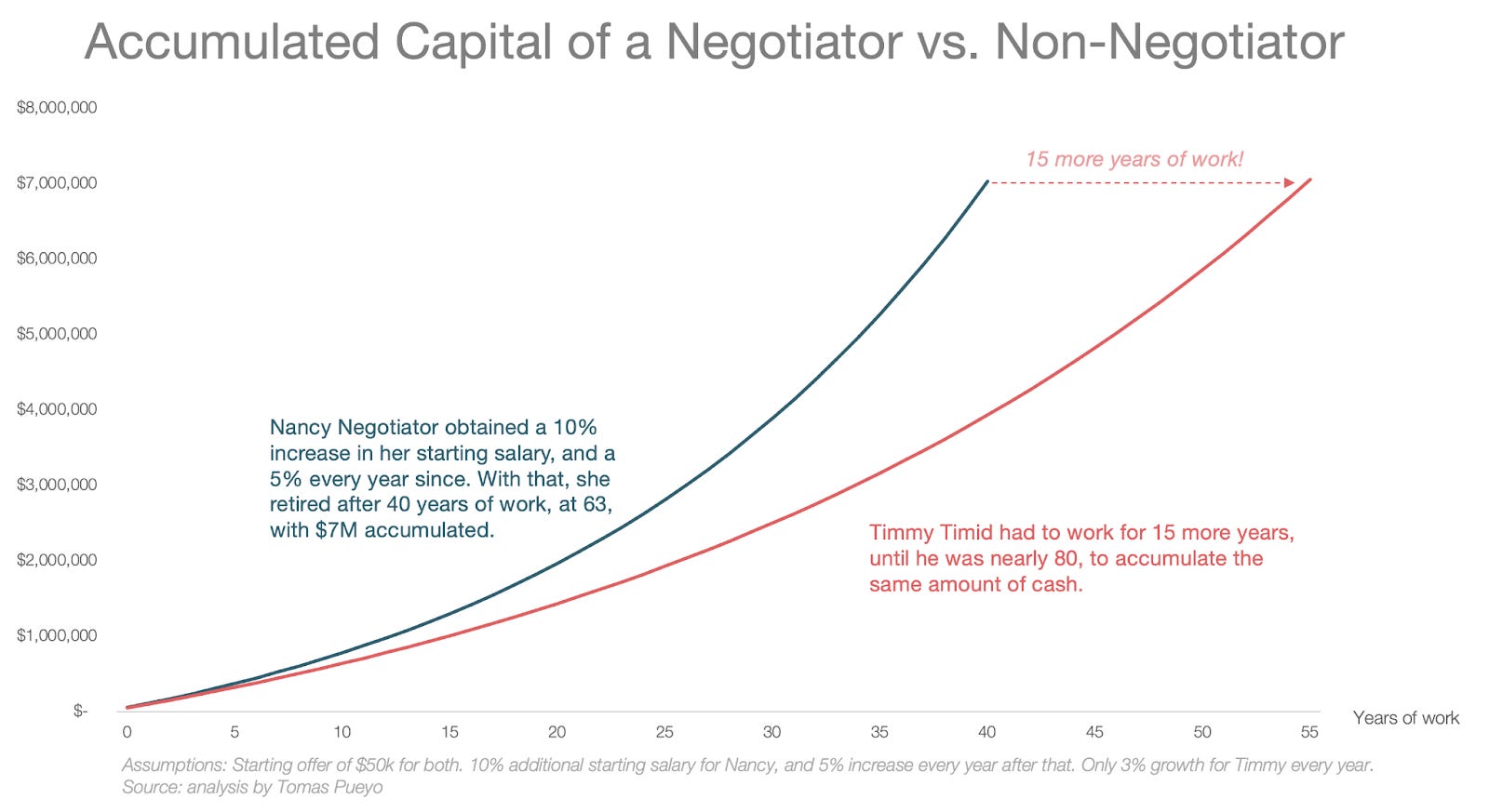

Imagine Nancy retires when she’s 63, after 40 years of work. How much longer does Timmy need to work to accumulate the same amount of cash? 15 years.

And this is with a very small difference of 3% vs. 5% in annual growths. If Nancy Negotiator gets 10% salary increases every year, Timmy Timid would need to work 55 years to accumulate the same cash!

I hope this shows how important negotiation is. Combine it with good investment management, and the result for your wealth will be explosive. You’ll be able to retire very early. How early though?

3. Fk Y Money: What’s Your Number?

When trying to predict when you’ll be able to retire, the key factor is how much money you need to accumulate by that point.

That number is called “fk y money”, or simply “FU money”: if somebody bothers you, you can say “FU, I’m out” and leave, since you are financially independent and aren’t dependent on anybody.

So what’s your FU money? It seems like a pretty important number to know, but most people don’t. So let’s calculate it.

The FIRE movement has something called “The 4% rule”: If your annual returns are 7% and inflation is 3%, every year your investments grow on average by ~4% in real terms. So if you only withdraw those 4% and live off of that, you will keep your money intact in the market, fighting off inflation.

Now you just need to know your annual spend to figure out how much money you need to accumulate in your investments.

If you need $80,000 to live, the 4% rule says you need to accumulate $2M [2] . These $2M will give you on average $140k per year, and you use $60k of that to fend off inflation. The rest is for you.

Personally, I prefer to take 3% to be more conservative, and I account for long-term capital gains, which take away 15% in the US. A person who needs $80k after taxes to live every year will need about $3.1M before retiring. So what’s your number?

4. The Accelerating Impact of Returns

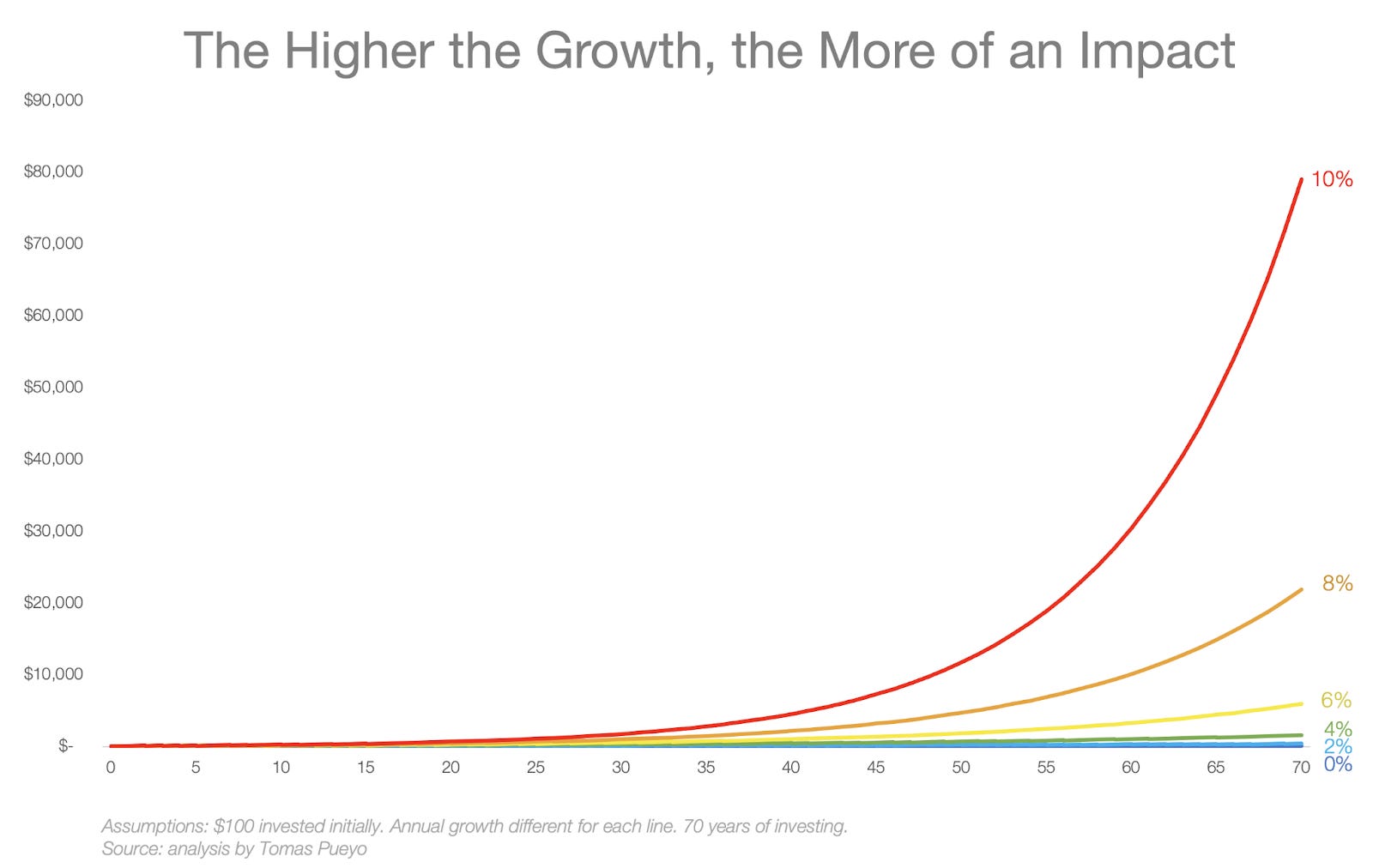

When talking about all these percentages, it’s easy to miss the different orders of magnitude.

One misconception might be: “Increasing my salary by 5% is already great. I won’t ask for 6 or 7%, that difference wouldn’t matter.” Or: “My assets are already growing at 4%. I don’t need to take more risk to make them grow at 6% or 7%.

Nothing is further from the truth. Going from 1% to 4% growth is a much smaller difference than going from 9% to 10% growth.

This has a big consequence: when managing your money, it’s good to take care of the big things like investing or negotiating. But the more things you optimize, the more you benefit from optimizing further, because at that point small changes in annual growth will have dramatic increases in wealth over time.

This should help understand the focus on fees, commissions, and taxes the other day. If your returns are 10% and your fees are 2%, you get knocked off from the 10% trajectory to the 8% trajectory from the graph above.

It’s like in epidemiology: a virus with an R0=2 is bad. R0=4 is much much worse. R0=6 is a nightmare [3] .

5. How Financial Advisors Create Urgency

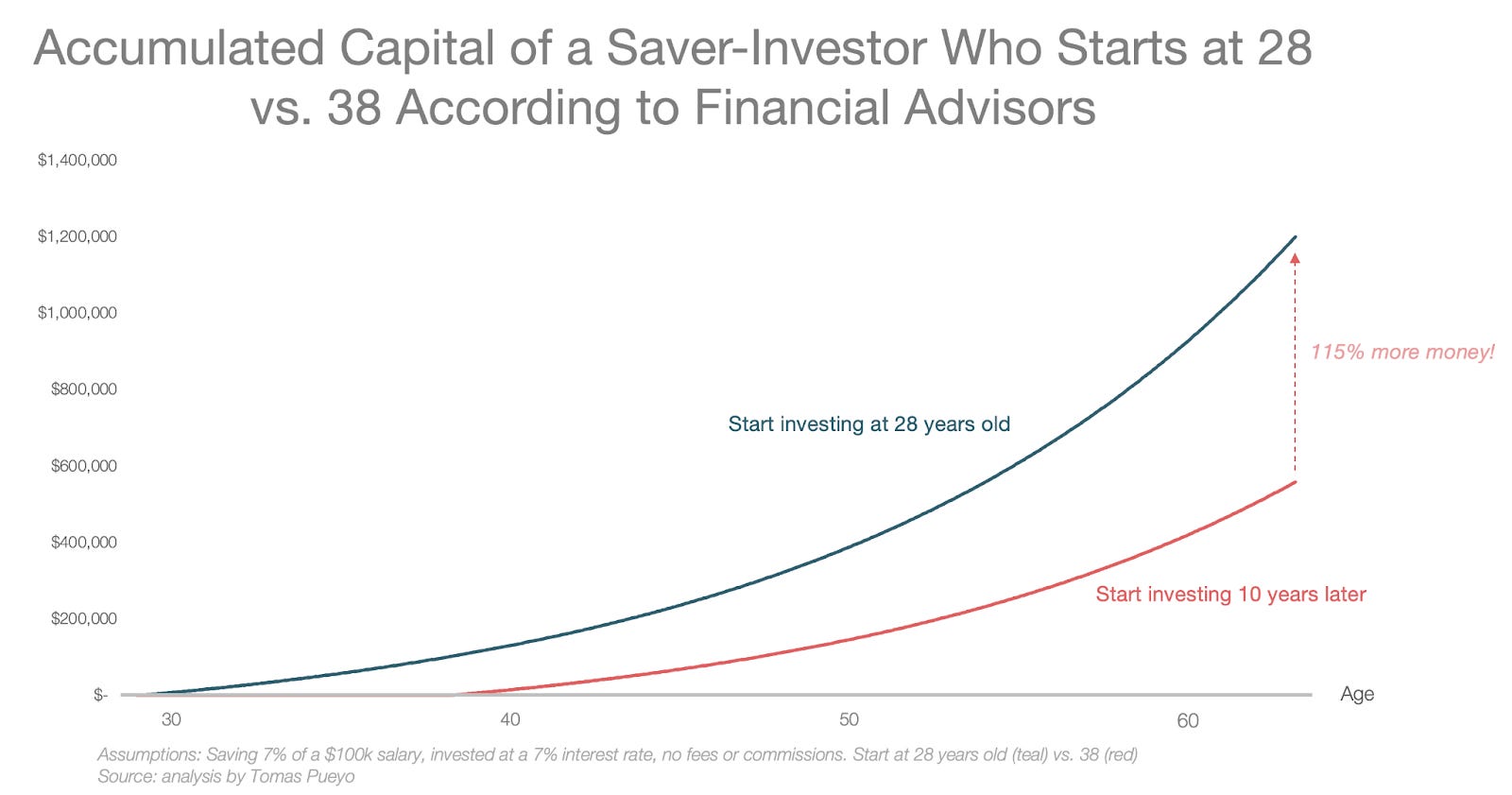

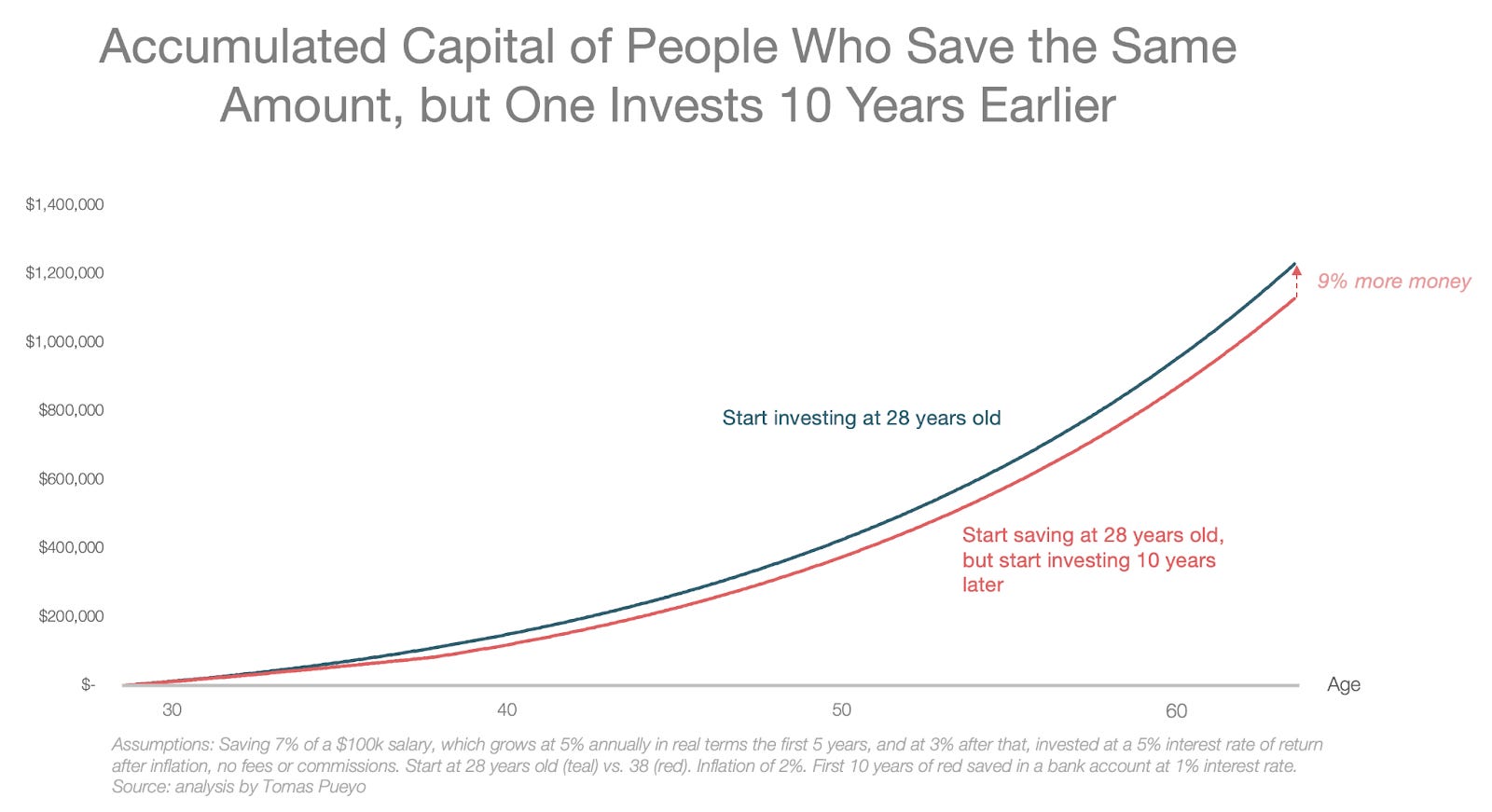

“The best moment to start investing was your first paycheck. The second best moment is today.”

This is the slogan of millions of financial advisors. They accompany it with a chart like this:

It’s true that the earlier you invest, the better it is for you. The problem with this chart is that it makes people feel like failures if they haven’t invested yet, when in fact it’s not too late.

The things that Financial Advisors conveniently forget are:

It’s not like those who invest later don’t save. They save, they tend to just not invest that money.

Incomes grow over time, so there’s less capacity for saving earlier on. They grow especially fast early on, so the savings from the first few years don’t amount to much.

It’s true that compounding accumulates money, but inflation undermines it. Investments that were made earlier have more time to depreciate. That somewhat modulates the impact.

So let’s add savings, income growth, and inflation [4] :

The difference shrinks from 115% to 9%. Now, 9% more money is a ton of money. You should definitely get on it asap! But don’t suffer terribly if you haven’t invested already. Just do it now.

6. Dollar-Cost Averaging

But when should you invest? Today? Maybe you’re scared because you hear the stock market is too high. If you invest today, you might lose everything if there’s a crash!

Two things. First, I’ve been hearing that the market is in a bubble since 2012.

A person who would have not invested in 2012 waiting for a crash would have missed out on doubling his money!

The same thing happened during COVID. Some people thought the stock market would crash…

Trying to avoid crashes is called “timing the market” and nobody can do that: if a person could, she would be the wealthiest person on earth. So what can you do?

Something called dollar-cost averaging [5] . Instead of investing everything at once, you move the money little by little. That way, if the stock market crashes tomorrow, you won’t lose a big chunk of your money, but you’ll still be somewhat exposed to the market.

Say you have $200k you want to move from your bank account to your investment account. How do you do that? Ask yourself what timeline you feel comfortable with for moving your money. Maybe six months? 1.5 years? Let’s take 1.5 years. Ok then, move a bit of money every month. Since there are 18 months, move about $11k every month from your bank account to your investment account.

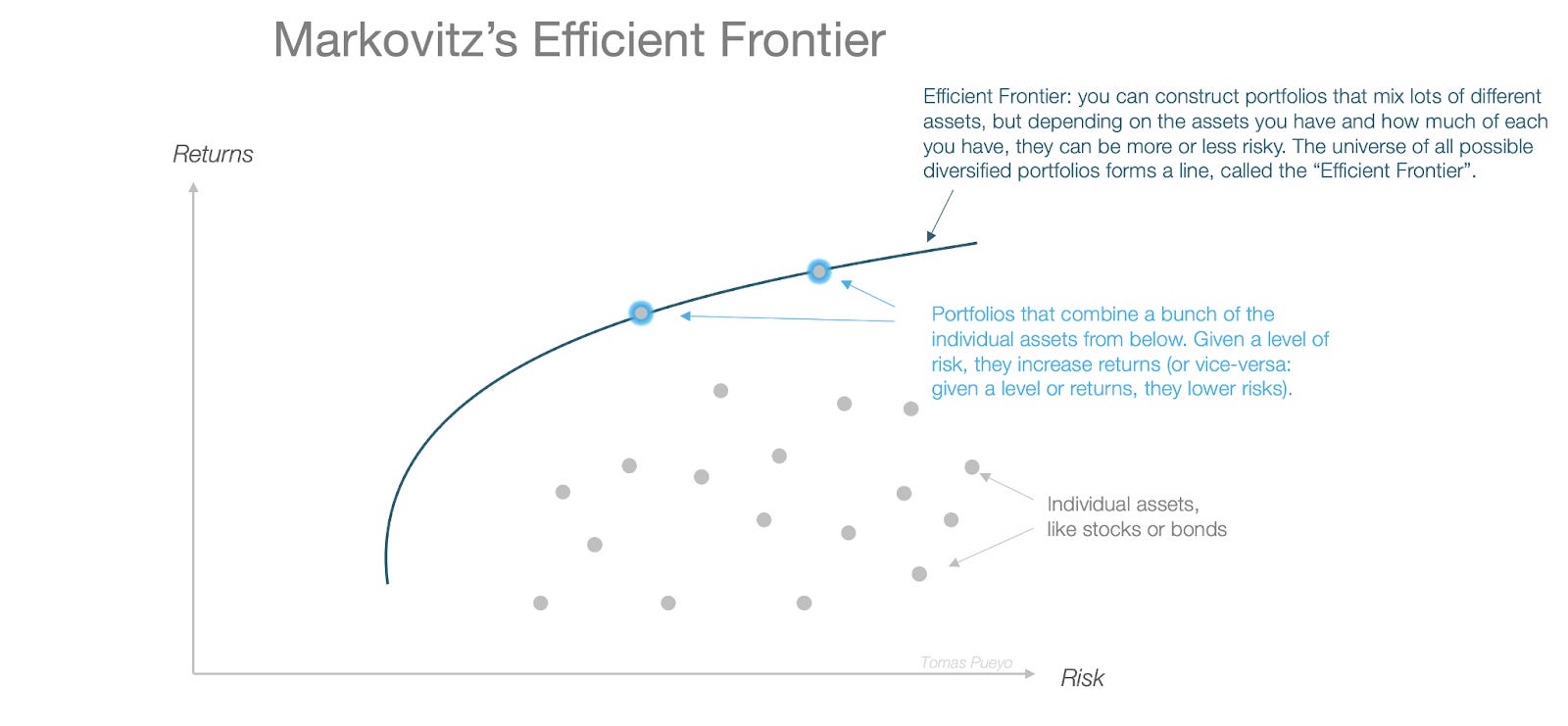

7. Markovitz’ Efficient Frontier

We said in the previous article that you should diversify your investments as much as possible because it could reduce your risk while keeping your returns. I mentioned a guy called Markovitz, who won a Nobel Prize for showing this. Let’s understand this better.

I offer you two deals. In one, you get a 50% chance to win $20,000, and a 50% chance to get $0. In the second, you get $10,000 for sure. Which deal should you pick?

The answer is the 2nd one, because it has the same expected return ($10k) but with no risk. With that confidence, you can plan your life accordingly. That predictability is valuable. So other things being equal, less risk is good.

Imagine instead of this deal, what I offer you is two investment options.

Invest $100 in a stock that might become $200 or stay at $100.

Invest $100 in a stock that will become $150 for sure.

For the same reason as before, you should pick deal 2.

Ok now for the key insight from Markovitz. Two new deals:

Like before, invest $100 in a stock that might become $200 or stay at $100.

Invest $50 in that stock, but also $50 in another stock. One of them will double in value, but you don’t know which one.

The 2nd deal is best for the same reason as before, because both deals have an expected value of $150, but the 2nd one will get to $150 with much higher confidence.

The key here is that two stocks won’t move together, so there’s a lot of value in getting investments that don’t grow at the same time because they cancel each other’s risk.

If instead of 2 stocks you buy hundreds of assets, you get an amazing diversification. And all the potential portfolios you could get this way are all very efficient, and form an “efficient frontier”.

The grey little bubbles are individual assets. They have a certain risk and return. But you start combining them into portfolios—the blue bubbles—and they suddenly have a higher return with the same level of risk (or a lower risk for the same return, it’s the same. They basically go up and to the left, which is good)

There’s an infinite number of blue bubbles, because you can combine the grey bubbles in an infinite amount of ways. These blue bubbles, together, form a line. That line is portrayed here in dark blue, and is called the efficient frontier.

You then can pick where in the efficient frontier you want your portfolio to be, depending on the risk you want [6] .

8. What Does Diversification Really Mean?

Ok, you’re convinced. Diversification is good. But what does that really mean in practice? How to you make your portfolio actually diversified in reality?

I talk all the time about index funds. These funds buy all the stocks from an index. For example, an S&P 500 index fund buys a bit of all the 500 underlying stocks in the S&P 500. But these companies are the largest ones in the US. That’s not great diversification! What about small companies? What about government bonds? What about stocks and bonds from abroad? What about real estate? Commodities? Cryptocurrencies?

The principle of diversification is this:

“I don’t know what will go up or down, so I’ll just do the average of all other investors out there.”

If there are $10T invested in our domestic stock market and $60T invested in foreign stocks, technically you should invest 1/7 of your stock investments in your domestic market and 6/7 abroad.

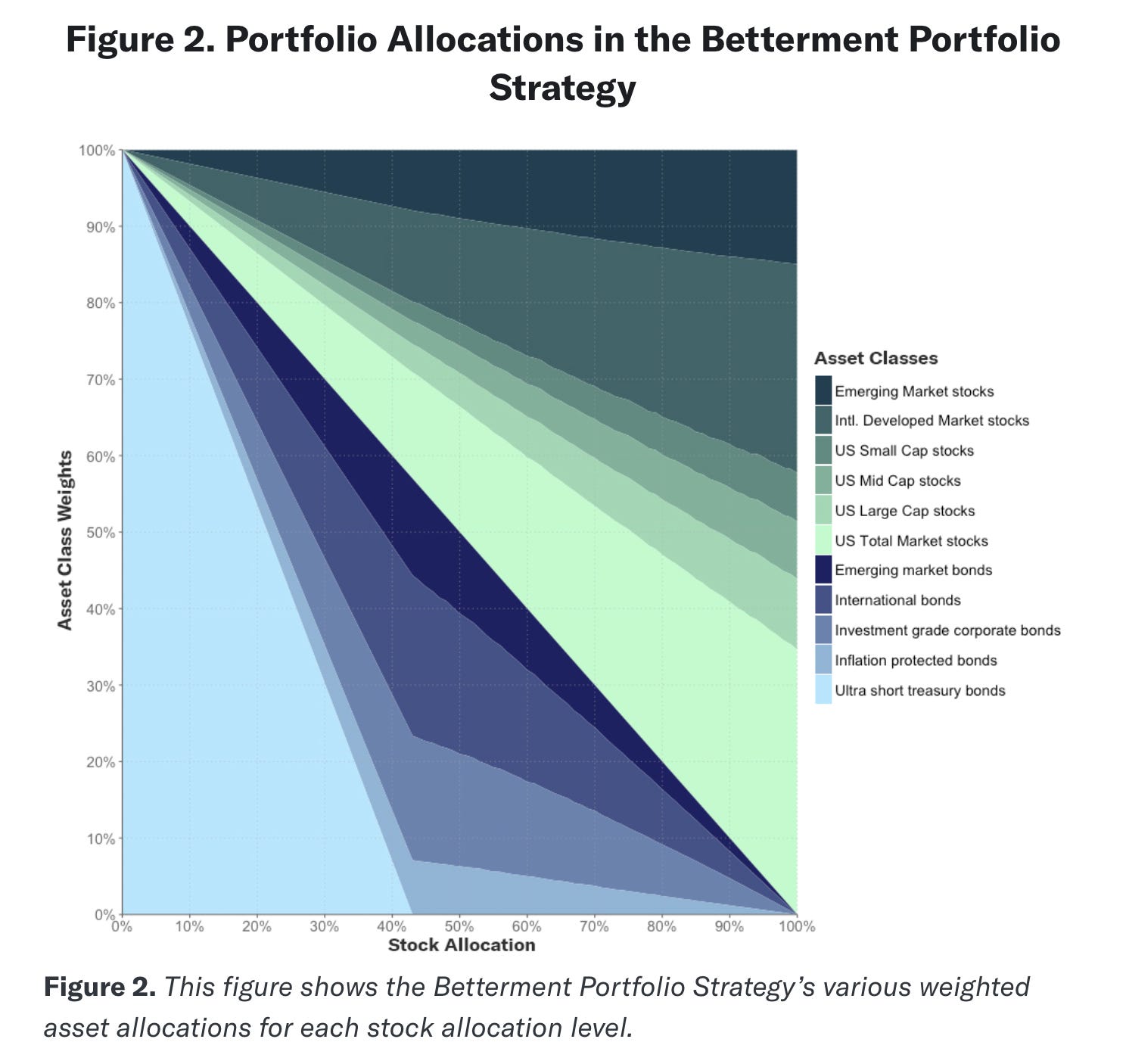

Roboadvisors follow this principle and create for you portfolios that are on the efficient frontier and very very diversified. You can see it in the investments they propose:

“US Stocks”, “Emerging Market Bonds”, “Commodities”... all of these are called “asset classes”, and to be properly diversified you need a bit of as many as possible.

Now investors get very angry about this, because if their home country’s investments are doing better than the world average, they feel like they’re missing out. Since the US has been on a tear over the last decade, this happens a lot in the US.

As a result, they overindex their home country. I’m ok with that, since the US is such a big country. But in general it’s good to invest across the world.

And stocks and bonds are not the only thing you should diversify on. What about cryptocurrencies?

9. Cryptocurrencies, Fiat Currencies, Modern Monetary Theory (MMT), and How They Affect All of This

As we’ve seen, two critical investment factors are inflation and asset classes. Cryptocurrencies are relevant because of both.

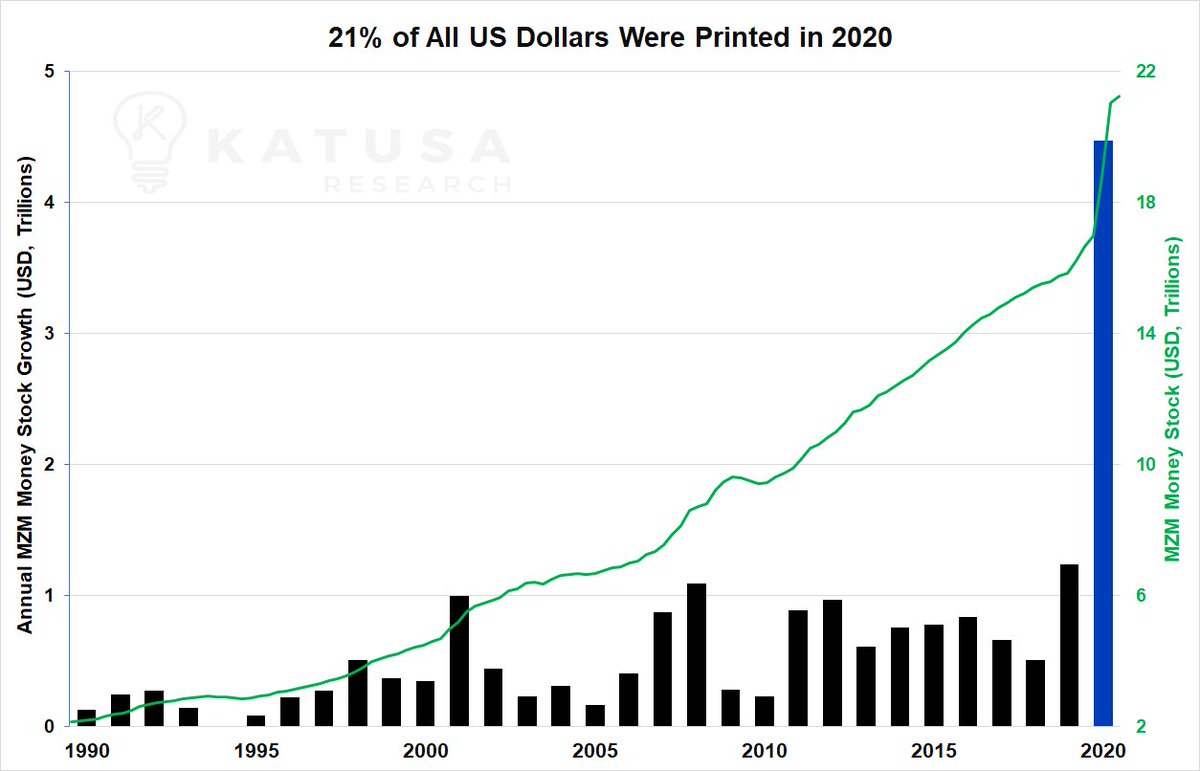

Bitcoin and its underlying technology—Blockchain—were created in the middle of the 2008-2009 Great Recession. The world was falling and governments started printing billions of dollars, euros, yens, and other currencies, to keep their economies afloat. Then, they realized something: inflation doesn’t appear to go up!

This was amazing for governments, because if they can print all the money they want with no consequences, they can spend whatever they want!

21% of US Dollars were printed in 2020 (so far), or $4.5 Trillion.

This is more than the amount of money created in the previous 5 years, yet only 5% of it is new cash in circulation.

Learn what this means - bit.ly/35KmWMF

@MarinKatusa

@SantiagoAuFund

Of course inflation exists, but those who control the printing press also control the inflation statistics (for now).

One way to look at it is according to Modern Monetary Theory. It says that money is just one more product, like oil, or TVs, or gold. It has some special properties (lasts a long time, fungible, not replicable by any but the government…), but it’s just a product that also responds to supply and demand. Supply a ton of money, and there’s more supply than demand, so the price of money goes down → there is inflation.

This would explain why printing so much money in the Great Recession didn’t have an impact in inflation: we had just destroyed trillions in real estate value. The supply of money was just filling that hole.

But governments might have taken the wrong lessons: “I can just print money with no consequences!” So they kept printing and printing… And then COVID came and they printed A LOT.

This didn’t happen with gold in the past because there’s only so much gold, but it did happen when gold or silver mines were discovered. It is argued that one of the reasons why Spain’s economy tanked after discovering America is because gold and especially silver created inflation. But creating more gold or silver is much harder than printing paper. That’s why people flocked to gold in times of inflation.

This is even more true for Bitcoin, because there’s only ever going to be 21 million Bitcoins. You know that because it says so in its code, and that code can’t be changed because of the blockchain—that’s the key technological innovation there.

As the world slowly realizes the value of Bitcoin, more and more people put some of their money in it, demand goes up, and with a fixed supply, price goes up.

Not all cryptocurrencies have a limited supply. For example, the other big cryptocurrency, Ethereum, doesn’t have a limited supply as of yet. But investors take cryptocurrencies as an asset class, and since they don’t know which ones will win, they simply buy a bit of the ones that look like the best bets.

I personally have some money in cryptocurrencies, and given the huge potential that they have, I think it’s an asset class that it makes sense to own. It has what’s called an asymmetric risk: it might go down, but if it goes up, it’s likely to go up a lot.

I don’t recommend it, but some people have all their wealth in them—and have made millions. In some cases, billions. Does that make sense?

10. When should you concentrate your bets?

This goes against what we just saw about diversification. Normally, the more you diversify, the better. But it’s important to remember why.

It’s because you don’t know what will win.

What if you did?

Well, if you knew that a stock is about to go from $100 to $110 with 100% confidence, you should sell your house, get all the loans you can, max out your credit cards, beg for money from everybody you know, and invest at $100. Imagine you gather $10M. Once the stock is at $110, you sell. You made $1M in profit. You give the money back, maybe with a 1% interest, and you pocker $900k. For some people, that’s FU money [7] .

Put in another way, with certainty comes bet concentration.

The problem is that this usually never happens [8] . Because if others knew the stock was going to go from $100 to $110, they would have already bought it and it would already cost $110. So you can’t be certain something will go up. What you can, however, is be contrarian and right.

You should concentrate your bets only if you’re very confident something’s going to go up AND most people disagree with you.

So why do people invest in cryptocurrency? Their thesis is the following one: “I see and understand the value of cryptocurrencies. But it’s complex. People aren’t used to a new asset class based on code. There’s math behind it. Also, accepting cryptocurrencies means accepting Bitcoin is better than gold, and cryptos are better than fiat money. Governments can’t do that easily, because they would relinquish their ability to print money. So as a result there’s plenty of laggards. Therefore I’m contrarian because I see something that most of the world doesn’t see yet.”

You can’t be 100% sure, so you shouldn’t invest all your money. But the higher the confidence, the more you should concentrate your bet.

Most of the biggest fortunes in the world have been made this way. George Soros when he piled on the British Pound’s peg on the European Exchange Rate Mechanism. Oil oligarchs. Robber Barons. Tech founders… All of them, highly concentrated in one bet that turned out to be right.

So don’t just blindly diversify everything. Diversify most of your money most of the time. If you want some play money for concentrated bets, do that. And if you blindly believe in something and most people disagree, consider making that bet with more money than usual. That’s the path to amazing wealth. It’s also the path to abject poverty though, so be very f****** sure it’s the right bet, and don’t put 100% of your wealth in that basket.

11. The Mental Biases that Make Active Investing Really Hard

Buy low and sell high, the unicorn rule of investment: everybody understands the concept but nobody can really experience it. Instead, people tend to buy high and sell low. Why?

If you trade in the market, think about your own investments. How do you do it?

First, there’s a stock you’re interested in. You start following it. But you’re not sure about it yet. You start seeing it grow. Some good news. Ok. maybe you should start investing. Then it grows some more. And you’re like “Sh*t, I’m missing out! I need to invest! All these other people are making money hand over fist! Am I going to be the last dumb schmuck working into my 70s?”

Except thousands have done exactly the same, and now the stock is overbought, and the price too high. You bought at the peak.

So others start selling. And you suddenly have some losses.

First you think: “Ok this is just a blip.”

Then it keeps going down. “I already lost $1k in this. I’ll stick until it goes back up and I reduce my losses.”

But then it keeps going down. “No! No! No no no no no… Sh*t, this is going to hell! I’m out.”

You sell.

At the bottom.

On the way up, you fell prey to the recency effect: you remembered the latest piece of news more than older news. That makes you buy expensive stocks because you’ve just heard something is doing well. It also makes you sell cheap stocks: You’ve heard something is losing value, so it might be time to sell.

There’s also confirmation bias and escalation of commitment. Once you buy, you’ve taken a stance. You made a forecast that something was going to go up. You took a position and wanted to remain consistent with it, so you didn’t quickly react to new information. You didn’t want to be proven wrong, so you hoped the downward trend was only temporary. Until the pressure was so high that you broke and sold cheap.

You can also find social proof. How many times do you hear people bragging about their amazing investments? And how many times do you hear them bragging about their terrible investment decisions? That’s right, there’s a massive survivorship bias: the stories you hear are those of the winners, because the losers keep quiet.

Linked to that is the Fundamental Attribution Error. Self-directed investors tend to bet on riskier-than-average stocks. So when the stock market is going well, they tend to do better than the market. Not because they’re geniuses, but because they are taking more risk. But they are prey to the fundamental attribution error, so they think they’re really good. They grow overconfident. If the market turns sideways, it’s never their fault. It’s the market who failed, who did what it wasn’t supposed to do.

There’s also issues of FOMO [9] , where you see others make a lot of money and tell yourself: “Damn, everybody around me is becoming so rich! Will I be the only one staying poor?” Or the issue of Authority, whereby you follow the advice of people you consider authorities. Which many other people also do. So they make the same investments. These are the exact opposite of being contrarian. Making concentrated bets following the herd is a sure way of investing your way to poverty.

Investing is so emotional, psychological, and counter-intuitive that only the most rational people sticking to rational approaches win. The only way to do this well is not to be fearless. It’s to understand the deep value of an asset better than others and compare it to its price, so you can figure out if something is underpriced or overpriced. This is super hard, so it’s either your job or you limit it only to a few companies that you know really well. And for most of your money, trust it to roboadvice algorithms or index funds, which are much more objective.

12. Specifics of Tax Optimization

We talked about reducing taxes earlier this week. But how?

This is not a guide for advanced tax optimizers, but rather the 80-20: the 20% of things that cover the 80% of most common tax optimizations. You can see it as an intro if you want.

Tax Optimization From Your Income

The first thing to do is to keep as much of your income as possible pre-tax. Different countries do this differently, but they tend to have solutions to do that for retirement and healthcare.

In the US, the most common ones are for retirement accounts like 401ks or IRAs (traditional, Roth, SEP, backdoor Roth IRAs), and health accounts (HSAs, FSAs).… Look into all of them. Read about them. Contribute to them. These are some of the best places to put your money. Their returns are eye-popping.

Say you live in California and make $100,000 a year. That puts you in the 35% tax bracket for federal + state income taxes. That means you keep $0.65 for every dollar you make. How long will it take you to grow those $0.65 back into $1, assuming a 5% return rate? Answer: 9 years. Every dollar for which you don’t pay taxes is a dollar for which you’ve saved 9 years of returns.

Health accounts are even less well understood than retirement accounts, but they’re quite powerful too. Imagine you need to spend $1,000 on healthcare this year. Paying this after taxes means you need to make around $1,500 before taxes in order to pay that $1,000 in healthcare.

Imagine instead you use a flexible spending account (FSA). Then you just spend that $1,000 before taxes. That’ll leave you with $500 pre-tax unused, which after taxes becomes $320. So you can save $320 on a spend of $1,000 just because you decided to manage your money through an FSA. Better, right?

If your employer has some matching program, such as a 50% 401k match, or covering 50% of your FSA, that’s free money and you should absolutely take advantage of that, as much as you can.

Tax Optimization from Your Investments

There are so many things to do say here that it’s hard to cover everything. I’ll cover only the basics.

Many developed countries have a difference in taxes between short term and long term. In the US, if you hold your investments for one year or more, you pay long-term capital gains taxes between 0% and 20%. But if you sell them within a year of buying, you pay as if it was normal income, which can go as high as 37%.

So all the trading that people do, buying and selling? Not only are they trying to time the market and are frequently not diversified enough. They’re also paying higher taxes. Better to diversify for the long term and only pay long-term capital gains.

Another trick is to do tax-loss harvesting: you sell the investments that have lost money to recognize losses. These losses will counterbalance other wins that you might have, canceling them out and pushing taxes down the road.

If you do that, you can’t buy back that investment immediately in the US. At least one month must have passed. This is the “wash sale rule”. Roboadvisors automate all this process by picking similar investments to the ones you sold, and automatically trading back and forth between them to recognize losses whenever they appear.

In general, robo-advisors are great at optimizing taxes, because code can do that really well: understand the rules, code how to work around them, and apply that over and over to all your accounts.

Another tool that especially rich people use is to never sell investments that have appreciated. If they sold them, they would have to pay taxes on the capital gains. Instead, they borrow money against them. That way they only pay the interest on the loans—which are very low right now—but not the taxes.

Imagine this scenario: you want to buy a $1M yacht. You sell $1.25M in investments, pay $250k in taxes, and are left with $1M to pay the yacht. You have one more yacht and $1.25M less in investments.

Instead, imagine you take a mortgage to pay for the yacht, backed by the stock. You now have a $1M yacht, you still have your $1.25M stock, and have a loan. But the loan only costs, say, 2%. It would take 11 years for the interests on that loan to add up to the $250k in taxes you’d have paid anyways—less in real terms—at which point your $1.25M in investments have likely increased in value. Rinse and repeat.

Tax is complex, so this is certainly an area where talking with an expert is worthwhile if you have a complex situation.

13. What parts of the work of a financial advisor can be automated

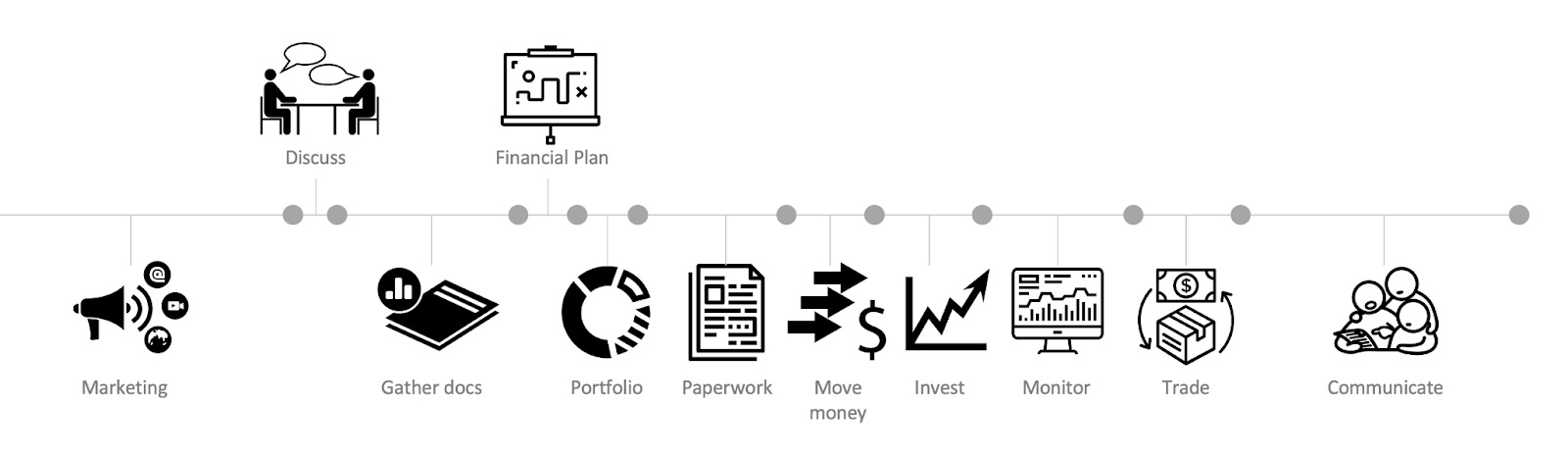

The work of a financial advisor, however, is pretty straightforward most of the time. Here are the components of a financial advisor’s role: they market their services so that people become interested in their services, they talk with them, gather their customers’ financial documentation, make a financial plan, build a portfolio to that translates the financial plan into actual investments, they do the paperwork to be able to execute the trades, they move the money into the investment account, invest it, monitor it, trade it when necessary, and communicate results with the customers.

Of all the services in this image, the bottom ones are better done when automated.

Who can better market their services: a single individual or a company with hundreds of millions of dollars of investments? Who can better trade: a human looking at the accounts of each one of their customers, or a computer? Who can better handle paperwork?

Who can better build high-quality portfolios that adjust to every situation: a single financial advisor that has to do a ton of them all the time, or a team of Finance PhDs working together to figure out the optimal response for each special situation?

The parts at the top are the only ones a human can do better than a robot. Discussing is obviously very human, and a good financial plan can take into consideration lots of edge cases that are difficult to code.

Today.

In the short term, the best of both worlds might not be a financial advisor on one side and a roboadvisor on another, but rather a financial advisor working with a roboadvice tool. In the long term….

14. What the People Working Inside the Roboadvice Industry Think about Their Products and How People Invest

As I’ve mentioned several times, I am biased. I worked in the roboadvice industry for years. There, I talked with professional financial advisors, people in competing companies, executives from traditional financial institutions…

From all these conversations, the takeaway was clear: roboadvice was by far the best solution for the vast majority of people.

The automation means there’s fewer workers to pay salaries to, so lower costs, which can be used to lower the price, so fees and commissions are cheaper.

Some of these cost savings can be spent on teams of finance and math PhDs, who can figure out the mathematically optimal solution for your investments. A financial advisor can never do that. They don’t usually have PhDs in finance.

Because trading is automated, it doesn’t fall prey to the mental biases we just discussed. They always do what’s mathematically right.

There’s also less opportunity for simple human error.

There are people for whom it’s not ideal. For example, people who need to do complex estate planning, who have cross-border investments, investments in tax havens… These high-stakes, complex situations are very hard for roboadvisors to model and automate a solution for, at least today, but in some cases maybe forever. Each situation is also unique, so all this modeling and automating work would be wasted. Clever, experienced, specialized financial advisors are great for that.

But for the vast majority of us? Roboadvice is the best.

It’s the main reason why big financial institutions jumped to the opportunity to deliver their own roboadvice solutions. Schwab built Intelligent Portfolios, Vanguard built its own tool, BlackRock bought Future Advisor, JP Morgan bought Nutmeg, Wells Fargo and UBS signed with SigFig…

Today, at least $400B in assets are managed by roboadvisors. Their progress was initially fast because early adopters love them. But they’ve since had to convince more traditional customers that this is an optimal solution, and that takes a long time. The same thing happened with Vanguard, which took decades to get where it is today, as more and more people have learned the value of index funds.

People are very conservative with their investments. It’s their hard-earned money. They don’t want to lose it! So they don’t quickly try new solutions. They prefer to look at a person face to face before entrusting their money. Hence the business of financial advisors, which will shrink for decades.

Most of the people who already figured out their investment strategies don’t want to revisit them. Vanguard grew as Baby Boomers discovered index funds. The same way, it’s likely that a generational replacement will be needed for automation to account for most of the financial advice that people need.

I hope you enjoyed this article too! I received a few super interesting questions following the last article. Feel free to ask me—or the rest of the community!—via comments or by sending me an email. I’ll answer the best questions in a future post!

For economic and moral reasons. The economic ones are obvious: lower costs. Morally, because happiness is not so much about having a lot, but rather desiring little.

80000/4%

The same can be said of Richter scales.

So let’s look at real instead of nominal wealth

Mathematically, once you’ve decided to invest, you should go all in and move your savings into investments. But this scares a lot of people, so this is a psychological trick that financial advisors use. Investing is mostly psychology anyways.

There are ways to beat the efficient frontier. Let me know if you’re interested and I’ll tell you.

Not you, big city dwellers who want to retire there. You were born to work forever until you can afford a 2 bedroom apartment.

One of the rare instances when this happens is with insider trading. You know your company is about to present results that are amazing, so you know the markets will react positively. Which is why so many ppl have become rich with it. It’s also why it’s penalized, because those who know this information, the workers of the company, are basically taking advantage of that information before shareholders. So they’re basically stealing from shareholders. Another way this is done is when politicians know a law will impact an industry once it’s made public. Hi Nancy.

Fear of Missing Out